Lenders are feeling the shift away from rate-induced boom times in mortgage. The total number of mortgage applications is down 57.6% as of July 8, compared to the same week of July 2021. Purchase apps are down 18.3%, but refinance apps are down 79.6%.

But are 2022 and 2023 projected to be as bad as headlines imply?

While there’s no way for lenders not to feel that shift, it’s the speed of change that has most impacted them. The industry has not seen rate increases of 75 basis points since before the turn of the century. It feels like a bust. But when the forecast tells a different story – one of a return to a purchase market that lenders have known and made profits in for decades.

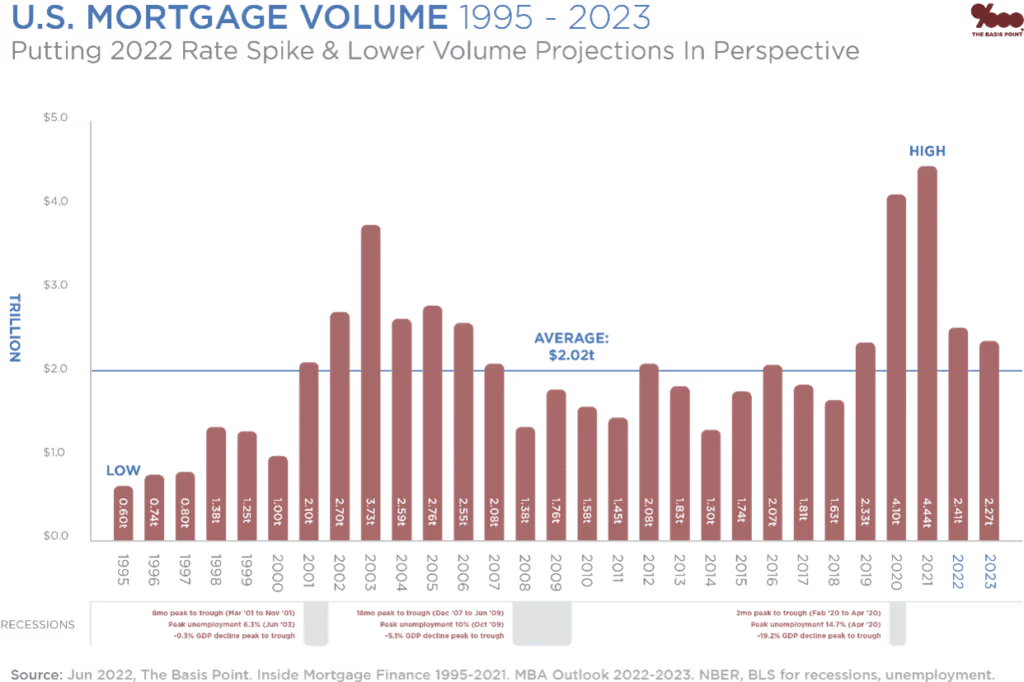

Economist projections are best guesses at what the market will do. If we assume the market offers volumes close to those expected by economists, then this year and 2023 will be above-average origination volumes. In fact, out of the 27 years from 1995 to 2022, only the period from 2002 to 2006 offered mortgage lenders more opportunity than economists now predict for 2022.

If the market does offer the 2.27 trillion originations projected for 2023, it will be a top-three, purchase-market year since 2006, only 2019 is in the same ballpark. (This assumes a “purchase year” is defined as a year in which refinances make up less than 50% of originations.)

Editor’s note – update July 22: Fannie Mae’s Economic and Strategic Research (ESR) Group adjusted its projections for 2022 total home sales growth to a decline of 15.6%, compared to a decline of 13.5% predicted last month. ESR also revised upward its home price appreciation forecast to 16.0 percent year-over-year-growth in 2022 from the previously projected 10.8 percent.

Equity – 2022’s Refinance Opportunity

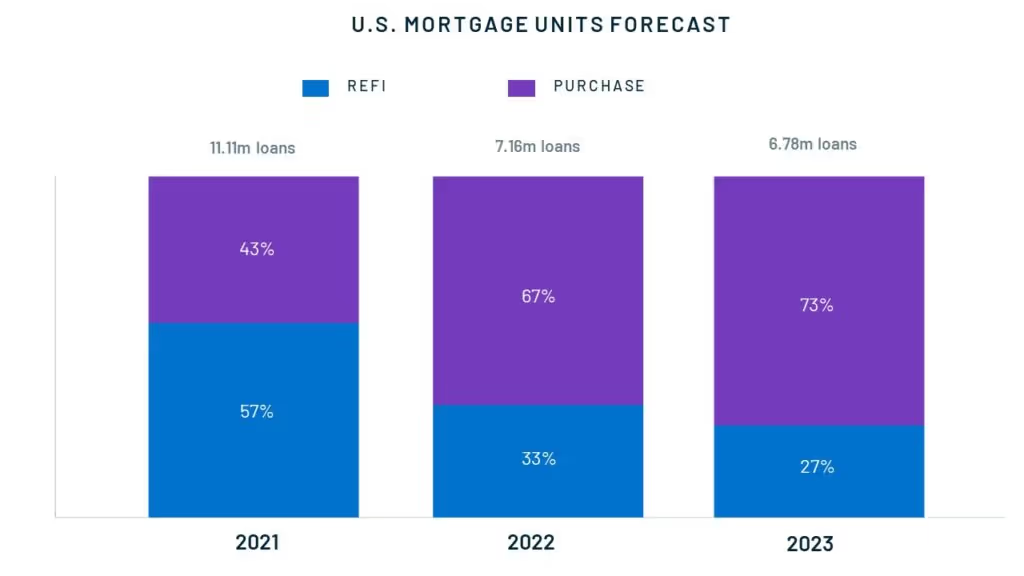

One important difference between 2022 and 2023, compared to other purchase years, is the remaining refinance volume available.

Most of the pain of declining rate refinances will be baked in by the end of 2022. After that, refinances will provide similar contributions to origination volumes in 2022 and 2023, according to economists’ crystal ball at least.

In fact, refinances are anticipated to remain at 33% and 27% in 2022 and 2023, respectively – even though few people can rate refinance anymore.

Homeowners’ record-setting equity is the reason is projected to provide significant strength to refinance volume.

Single-family home prices increased at the annualized rate of 19.4% in second quarter of 2022, down slightly from the previous quarter’s 20.5%, according to Fannie Mae.

“Home prices maintained a near-historic pace of appreciation in the second quarter, as low levels of housing inventory continued to support price growth,” said Doug Duncan, Fannie Mae Senior Vice President and Chief Economist. “At the end of 2021 and extending into 2022, we believe many homebuyers pulled forward their purchase plans to avoid expected increases in mortgage rates, contributing to demand for homes and strong price appreciation.”

Fannie Mae economists expect the sharp rise in mortgage rates to cool purchase demand in the quarters ahead, which in turn will moderate home price appreciation. Equity growth is predicted to slow. Yet, homeowners are forecast to both keep and to grow their equity in the years to come – many projections still put that equity growth in double-digits for 2022.

The Mortgage Relationship Moment

As noted by Fannie Mae’s Chief Economist, rates are motivating buyers to move this year before rates climb even more. Homebuyers need lenders who have the expertise and the tools to help them into their next home as soon as possible. With bond markets signaling a rate increase of 75 basis points, if not a full percentage point in July 2022 (at the time this guide was published), borrowers need help figuring out what to do, and they need it fast.

Consumers are increasingly pessimistic about their prospects in home real estate. Their sentiment about homebuying conditions fell to its second-lowest reading in a decade, according to a Fannie Mae report on Home Purchase Sentiment.

If buyers are downtrodden on the market, you might expect sellers to be optimistic. But that’s not what Fannie Mae found. The percentage of consumers who believe it’s a “Good Time to Sell” fell to 68% – a decline of 10% this month. For the first time since 2015, approximately half of all respondents indicated that it would be ‘difficult’ to get a mortgage, the highest such percentage since 2014. People feel uncertain. Both buyers and sellers aren’t sure they can afford a new home with prices and rate appreciating at the same time.

Homebuyers’ negative sentiment, though, shouldn’t be read as defeat for the mortgage and real estate market. The majority of consumers in the same survey said they would prefer to buy a home if they moved, rather than renting. People want to own a home; they’re just not sure they can manage to get into one. They need a provider who knows the steps to make their goals possible.

The same is true for homeowner who have equity. Many can get out of debt, others can finally upgrade their home, and still more can pay for unexpected large expense without using a credit card. They need to know and understand their options; they await a lender who will show them.